Opinion on financial statements of Bodycote plc

In our opinion:

- the financial statements give a true and fair view of the state of the Group's and of the Parent company's affairs as at 31 December 2014 and of the Group's profit for the year then ended;

- the Group financial statements have been properly prepared in accordance with International Financial Reporting Standards (IFRSs) as adopted by the European Union;

- the Parent company financial statements have been properly prepared in accordance with United Kingdom Generally Accepted Accounting Practice; and

- the financial statements have been prepared in accordance with the requirements of the Companies Act 2006 and, as regards the Group financial statements, Article 4 of the IAS Regulation.

The financial statements comprise the Consolidated Income Statement, the Consolidated Statement of Comprehensive Income, the Consolidated and Company Balance Sheets, the Consolidated Cash Flow Statement, the Consolidated Statement of Changes in Equity, the Statement of Group and Company Accounting Policies and the related notes 1 to 29 and 1 to 11 for the Group and Company financial statements respectively. The financial reporting framework that has been applied in the preparation of the Group financial statements is applicable law and IFRSs as adopted by the European Union. The financial reporting framework that has been applied in the preparation of the Parent company financial statements is applicable law and United Kingdom Accounting Standards (United Kingdom Generally Accepted Accounting Practice).

Going concern

As required by the Listing Rules we have reviewed the directors' statement that the Group is a going concern. We confirm that:

- we have concluded that the directors' use of the going concern basis of accounting in the preparation of the financial statements is appropriate; and

- we have not identified any material uncertainties that may cast significant doubt on the Group's ability to continue as a going concern.

However, because not all future events or conditions can be predicted, this statement is not a guarantee as to the Group's ability to continue as a going concern.

Our assessment of risks of material misstatement

The assessed risks of material misstatement described below are those that had the greatest effect on our audit strategy, the allocation of resources in the audit and directing the efforts of the engagement team:

| Risk | How the scope of our audit responded to the risk |

|---|

| Impairment of non-current assets | |

| Given the Group's significant asset base and the continued macro-economic uncertainties in certain global territories, this risk concerns the carrying value of intangible (including goodwill) and tangible fixed assets. The Group's assessment of the carrying value of intangible and tangible fixed assets of £172.1m and £434.6m respectively requires significant judgement, as described in note 10 and the key sources of estimation uncertainty within the accounting policies. Particular attention is given to cash flow, growth rates, discount rates and sensitivity assumptions. | We challenged the assumptions used in the impairment model for intangible and tangible assets. As part of our procedures we:

- considered the appropriateness of the growth rate assumptions by comparing them to historical trading performance for both revenue and operating profit across the Group's geographical and market segments;

- assessed the appropriateness of the assumptions concerning inputs to the discount rate against latest market expectations. In performing our procedures, we used our internal valuation specialists and third party evidence to assess the appropriateness of the discount rate applied; and

- considered management's assertions of the future utilisation of assets supporting their carrying value by reviewing the strategic plan for the business by cash generating unit.

|

| Environmental provisions | |

| Given the nature of the Group's operations, a risk arises in connection with the appropriateness and completeness of the £14.0m (2013: £13.8m) environmental provisions, in particular, their judgemental nature relative to the likely period of utilisation as described in the critical judgements within the accounting policies. The risk arises predominantly within the US component. | We evaluated the environmental provisions by comparing the basis for the recognition of provisions against the regulatory and legal requirements, assessing the value of the provision recognised and challenging the status and utilisation of provisions. As part of our audit procedures we reviewed third party evidence and assumptions detailing the assessment of environmental liabilities for the Group together with correspondence from the Group's internal environmental remediation team. As part of these procedures we also challenged the qualifications of management's experts. Where applicable, we also verified environmental provisions to regulatory and legal correspondence. |

| Taxation |

| The tax risk concerns the judgements and estimates applied in the determination of tax balances, in particular in relation to the recognition of deferred tax assets for tax losses across the Group as disclosed in note 19 and provisions for liabilities attributed to specific uncertain tax positions linked to the Group's complex corporate structures. | In conjunction with our taxation audit specialists, we have assessed and challenged the appropriateness of management's assumptions and estimates in relation to the likelihood of generating future taxable, as opposed to accounting, profits to support the recognition of deferred tax assets by comparing to forecast information and historical trends in loss utilisation. We have also assessed the assumptions and judgements concerning the adequacy of tax provisions for uncertain tax positions by viewing the latest correspondence from the various tax authorities and drawing on the experience of our tax specialists in respect of similar situations. |

| Pensions |

| This risk concerns the appropriateness of actuarial assumptions in calculating the Group's IAS 19 gross liability of £129.5m (2013: £108.7m). The valuation of the Group's IAS 19 deficit involves significant judgement as described in note 29 and in the key sources of estimation uncertainty in the accounting policies, in particular in relation to the discount rate, inflation and mortality assumptions. | We have assessed the appropriateness of the assumptions underpinning the valuation of the scheme liabilities. Specifically we challenged the discount rate, inflation and mortality assumptions applied in the calculation by using our internal pension specialists to benchmark the assumptions applied against comparable third party data and assess the appropriateness of the assumptions in the context of the Group's own position. |

The description of risks above should be read in conjunction with the significant issues considered by the Audit Committee.

Our audit procedures relating to these matters were designed in the context of our audit of the financial statements as a whole, and not to express an opinion on individual accounts or disclosures. Our opinion on the financial statements is not modified with respect to any of the risks described above, and we do not express an opinion on these individual matters.

Our application of materiality

We define materiality as the magnitude of misstatement in the financial statements that makes it probable that the economic decisions of a reasonably knowledgeable person would be changed or influenced. We use materiality both in planning the scope of our audit work and in evaluating the results of our work.

We determined materiality for the Group to be £4.9m (2013: £6.8m), which is below 5% (2013: 7.5%) of pre-tax profit, and below 1% (2013: 1%) of equity. We have reduced the percentage applied to pre-tax profit to align more closely with comparable companies.

We agreed with the Audit Committee that we would report to the Committee all audit differences in excess of £145,000 (2013: £145,000), as well as differences below that threshold that, in our view, warranted reporting on qualitative grounds. We also report to the Audit Committee on disclosure matters that we identified when assessing the overall presentation of the financial statements.

Revenue

Profit before tax

An overview of the scope of our audit

Our Group audit was scoped by obtaining an understanding of the Group and its environment, including group-wide controls, and assessing the risks of material misstatement at the Group level.

In 2014 we have continued to have direct Group oversight, leadership and control over the components in the Shared Service Centre (SSC) in Prague and the USA. We have further redesigned our audit work and the shape of the audit teams as more components have transitioned into the SSC. Consistent with the prior year and as agreed with the Audit Committee, the smaller components in territories such as China, Singapore and Mexico have remained in scope and we have maintained the scoping levels in territories such as Brazil, the Netherlands, Luxembourg, Germany and Turkey which were increased in 2013.

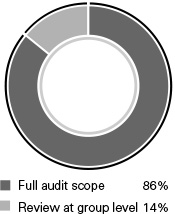

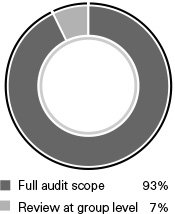

As a consequence of the audit scope determined, we achieved coverage of approximately 86% of revenue, 97% of profit before tax and 88% of net assets. Our audit work at each location was executed at levels of materiality applicable to each individual entity which was lower than group materiality. Component materiality ranged from £0.5m to £2.9m.

The Group audit team continued to follow a programme of planned visits that has been designed so that a senior member of the Group audit team visits each of the locations included as full scope for the Group audit at least once every three years and the most significant of them at least once a year. In years when we do not visit a significant component we will include the component audit team in our team briefing, discuss their risk assessment, attend close meetings by conference call and video conferencing and review documentation of the findings from their work.

Opinion on other matters prescribed by the Companies Act 2006

In our opinion:

- the part of the Directors' Remuneration Report to be audited has been properly prepared in accordance with the Companies Act 2006; and

- the information given in the Strategic Report and the Directors' Report for the financial year for which the financial statements are prepared is consistent with the financial statements.

Matters on which we are required to report by exception

Adequacy of explanations received and accounting records

Under the Companies Act 2006 we are required to report to you if, in our opinion:

- we have not received all the information and explanations we require for our audit; or

- adequate accounting records have not been kept by the Parent company, or returns adequate for our audit have not been received from branches not visited by us; or

- the Parent company financial statements are not in agreement with the accounting records and returns.

We have nothing to report in respect of these matters.

Directors' remuneration

Under the Companies Act 2006 we are also required to report if in our opinion certain disclosures of directors' remuneration have not been made or the part of the Directors' Remuneration Report to be audited is not in agreement with the accounting records and returns. We have nothing to report arising from these matters.

Corporate Governance Statement

Under the Listing Rules we are also required to review the part of the Corporate Governance Statement relating to the company's compliance with ten provisions of the UK Corporate Governance Code. We have nothing to report arising from our review.

Our duty to read other information in the Annual Report

Under International Standards on Auditing (UK and Ireland), we are required to report to you if, in our opinion, information in the Annual Report is:

- materially inconsistent with the information in the audited financial statements; or

- apparently materially incorrect based on, or materially inconsistent with, our knowledge of the Group acquired in the course of performing our audit; or

- otherwise misleading.

In particular, we are required to consider whether we have identified any inconsistencies between our knowledge acquired during the audit and the directors' statement that they consider the Annual Report is fair, balanced and understandable and whether the Annual Report appropriately discloses those matters that we communicated to the audit committee which we consider should have been disclosed. We confirm that we have not identified any such inconsistencies or misleading statements.

Respective responsibilities of directors and auditor

As explained more fully in the Directors' responsibilities statement, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board's Ethical Standards for Auditors. We also comply with International Standard on Quality Control 1 (UK and Ireland). Our audit methodology and tools aim to ensure that our quality control procedures are effective, understood and applied. Our quality controls and systems include our dedicated professional standards review team and independent partner reviews.

This report is made solely to the company's members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company's members those matters we are required to state to them in an auditor's report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company's members as a body, for our audit work, for this report, or for the opinions we have formed.

Scope of the audit of the financial statements

An audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the Group's and the Parent company's circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the directors; and the overall presentation of the financial statements. In addition, we read all the financial and non-financial information in the Annual Report to identify material inconsistencies with the audited financial statements and to identify any information that is apparently materially incorrect based on, or materially inconsistent with, the knowledge acquired by us in the course of performing the audit. If we become aware of any apparent material misstatements or inconsistencies we consider the implications for our report.

Nicola Mitchell (Senior statutory auditor)for and on behalf of Deloitte LLP

Chartered Accountants and Statutory Auditor

Manchester United Kingdom

26 February 2015